A whole subsection of the International media exists to tear at Tesla Motors. That’s part of the court of public opinion, the variety of “facts” tossed around that are really interpretations of the information we all receive. This afternoon Tesla released their quarterly financial results, and we don’t have to look at the resulting news articles to know there is a chorus of articles claiming that Tesla Motors is about to go bankrupt because they’re flailing away at ramping up production, and the company will run out of money.

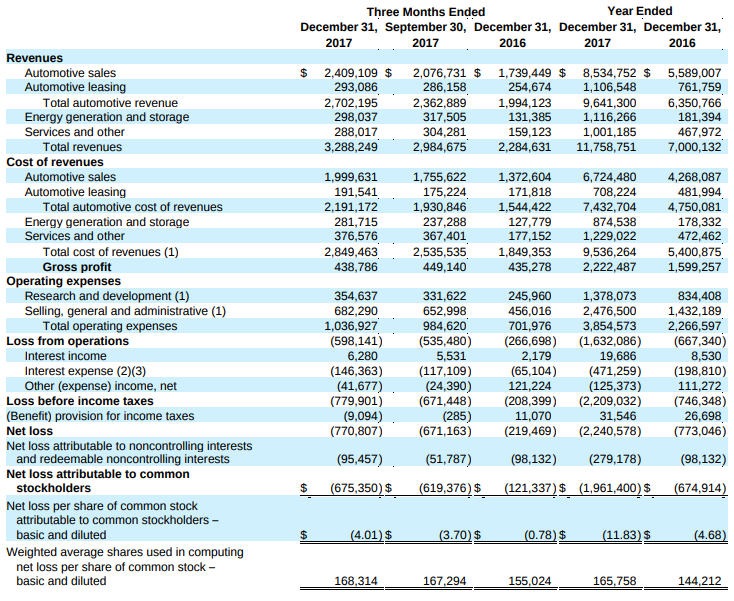

Tesla did announce $675 million in loss for the quarter, and nearly $2 billion in loss for fiscal year 2017, a fact which raises a few eyebrows. However what most of that chorus of naysayers are missing is the cause of that so-called “loss”, and why it should really be seen as an investment in the future.

I’ve written this same article several times now, so see:

- Tesla Motors could be profitable today, at the cost of a slower business plan

- Tesla Motors ready to be profitable again now that Model X is in production

- Lutz says Tesla Motors dying, Musk needs to cut costs adopt plug-in hybrids

- Is Tesla losing $4000 per car sold? Nope, it’s capital investment for future sales

- Tesla Motors doesn’t look like company gobbling at the public tax dollars trough

- Tesla Motors nearly died in 2013, sought Google buyout

The message today is the message I’ve written several times:

|

Sponsored |

- Tesla’s sales and revenue is growing strongly

- The “Net Loss” figure is “Revenue – Expenses”.

- Tesla Motors is obviously seeing high expenses because they’re building R&D and Factory/Production capacity in pursuit of the steep ramp-up in Model S/X/3 production

- Alongside these high expenses is growth in Assets – namely in factories and production equipment

In other words, Tesla Motors is investing in factories and parts and research in order to manufacture products and develop future products. That costs money. The company, for better or for worse, is moving at a hugely aggressive schedule. That costs money. It also costs in human capital — all those departures from the engineering department could be due to burnout. In any case, we’re focusing on financials, and the point is that an aggressive schedule of building the company means the “Revenue – Expenses” equation is currently resulting in a negative number.

But – as a good capitalist organization, what’s supposed to result is a future increase in revenue due to a future increase in sales. Indeed, Tesla’s revenue has grown quickly over the years. Their business plan (both versions) is posted clearly on the company website, and clearly states the plan is to plow revenues into aggressively growing the business and moving towards mass-market production of electric vehicles and other clean energy technology.

UPDATE — a day or two after Tesla announced these financial results, the company also pushed back Tesla Model 3 delivery estimates. This has angered many Model 3 customers and raises the possibility of a revolt among the fan base. For more see: Tesla delays deliveries angering large number of fans, destroying credibility?

These are the financial results from the Shareholders letter released today. You’ll see total revenues FY2017 of nearly $12 billion, and FY2016 of $7 billion. By any measure that’s a rapid increase in revenue.

There is a gross profit all along, meaning that Revenue – Cost of Revenue is strong. Where the “loss” occurs is when you add in Operating Expenses.

The Interest Expense is another item of worry, since that’s money paid out to investors. That grew considerably from 2016 to 2017. Tesla’s ability to continue as a going concern will depend on their ability to repay debtors and investors. Currently that expense looks acceptable, it’s about 1/4th the Operating Expenses for example.

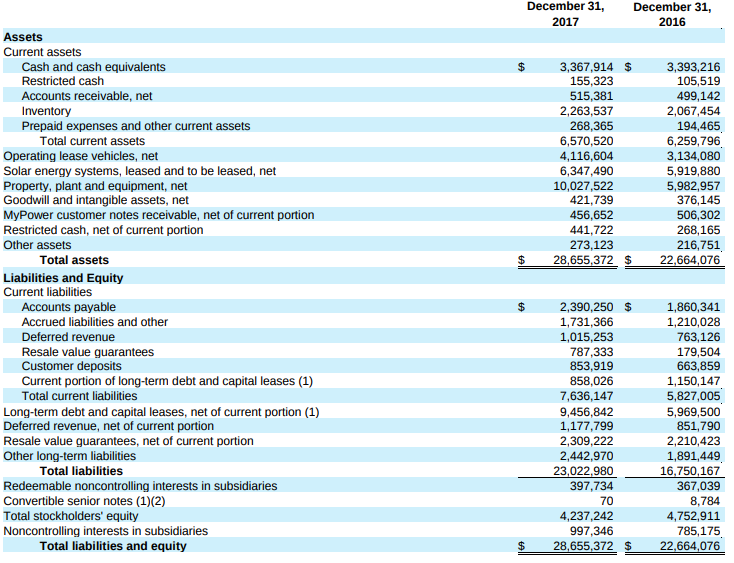

As I said – the costs are resulting in an increase in assets, specifically in factories and production equipment. Notice the line “Property, plant and equipment” and that between FY2016 and FY2017 that figure went from $6 billion to $10 billion.

THAT is where Tesla is putting their money. They’re building a manufacturing business.

|

Sponsored |

As is said in the shareholder’s letter – Tesla is seeking to be the most advanced automobile manufacturer in the world. They’re installing advanced equipment in their factories, and they’ve bought companies which specialize in factory automation.

You can see the cost for that equipment and employees in the financials. And, you can see the growing asset base in the financials.

Maybe the growing debt load will cause a problem. Capitalist economics theory says that so long as the company successfully expands their production, and so long as they successfully grow the sales and customer base, that such a company can pay off its debts and show a profit eventually.

The rollout of the Model 3, the Tesla Semi, the Gen2 Tesla Roadster, and the Tesla Energy products, are all critical to whether Tesla the company survives or crashes.

- The USA should delete Musk from power, Instead of deleting whole agencies as he demands - February 14, 2025

- Elon Musk, fiduciary duties, his six companies PLUS his political activities - February 10, 2025

- Is there enough Grid Capacity for Hydrogen Fuel Cell or Battery Electric cars? - April 23, 2023

- Is Tesla finagling to grab federal NEVI dollars for Supercharger network? - November 15, 2022

- Tesla announces the North American Charging Standard charging connector - November 11, 2022

- Lightning Motorcycles adopts Silicon battery, 5 minute charge time gives 135 miles range - November 9, 2022

- Tesla Autopilot under US Dept of Transportation scrutiny - June 13, 2022

- Spectacular CNG bus fire misrepresented as EV bus fire - April 21, 2022

- Moldova, Ukraine, Georgia, Russia, and the European Energy Crisis - December 21, 2021

- Li-Bridge leading the USA across lithium battery chasm - October 29, 2021

Pingback: Tesla delays deliveries angering large number of fans, destroying credibility? | The Long Tail Pipe

Pingback: Tesla Motors versus the other Car Makers and the future of the Car industry | The Long Tail Pipe