Since the Tesla Motors conference call for Q2 2015 quarterly results, the TSLA stock price has fallen from $270/share to $242/share. While we’re talking about a highly volatile startup company, the news in those quarterly results was not so good. A deep quarterly loss thanks to steep capital expenses related to rolling out Tesla Model X production made many take a deep breath, but the straw which broke the camels back was the scaling back of sales expectations. And then, following the conference call, Tesla Motors filed a registration with the SEC to sell more shares to raise capital.

Many are probably thinking something like this:

WTF? Is Tesla about to crater, and they need an emergency cash injection to avoid bankruptcy?

The primary risk to the business is Tesla Motors’ cash position.

- Sep 30, 2014: $2.388 billion

- Dec 31, 2014: $1.923 billion

- Mar 31, 2015: $1.530 billion

- July 31, 2014: $1.171 billion

That’s a pretty steady rate of cash erosion, $400 million per quarter, meaning the company has less than 3 quarters of cash on hand. At the same time total assets have grown from $5.437 billion to $6.468 billion over the same time period. That’s due to a growth in inventory ($752 million to $1.212 billion) and Property/plant/equipment ($2.022 billion to $3.766 billion) over the same time period.

As we noted previously – In this phase Tesla Motors is building factory capacity to build new products – the Tesla Model X and the Tesla Energy products. That means spending cash, building stuff, and later they’ll earn a return on the investment by selling enough stuff to pay for everything.

On its current product line (primarily the Model S) Tesla Motors revenue grew from $851 million to $954 million over the same time period. Cost of Revenue is less than the revenue, meaning there was a gross profit but it fell from $251 million to $213 million over the same time period. That’s not a good sign for revenue to grow but cost of revenue to grow even faster. In any case R&D and administration expenses are steep enough to give Tesla Motors a significant operating loss which grew from $39 million to $170 million over the same time period.

Among the current revenue sources is battery packs and other components for the Mercedes-Benz B-Class Electric. That car uses Tesla stuff under the hood, but it was just announced that Daimler canceled the project and will produce those components in-house . So… the revenue picture just got a little worse. How much? Tesla doesn’t break out revenue from Daimler, but it’s included in the $76 million row labeled “Services and other” which includes any services provided to other manufacturers as well as the Tesla Energy products. The Q2 2015 10Q says there’d been increasing costs for the Daimler revenue, so losing this deal could be a blessing in disguise by cutting a large expense.

. So… the revenue picture just got a little worse. How much? Tesla doesn’t break out revenue from Daimler, but it’s included in the $76 million row labeled “Services and other” which includes any services provided to other manufacturers as well as the Tesla Energy products. The Q2 2015 10Q says there’d been increasing costs for the Daimler revenue, so losing this deal could be a blessing in disguise by cutting a large expense.

On the other hand, Daimler is doing this to set the stage for 500 kilometers range (300 miles) in an upcoming version of the B-Class. Meaning that Daimler has switched from owning a chunk of Tesla Motors, and partnering with the company on drivetrain components, to going into competition against Tesla Motors after selling out their holding.

|

Sponsored |

Until the Q2 results conference call the “guidance” (prediction) from Tesla Management was that they’d deliver 55,000 vehicles (Model S and Model X) during 2015. In the conference call we were advised the deliveries would be between 50,000 to 55,000 vehicles. A large chunk of those vehicle deliveries are to occur in Q4 when the Tesla Model X production ramps up.

During the conference call Elon Musk described the Model X as perhaps the most complicated car ever built – ergo, we’re expecting they’re having some trouble getting the falcon wing doors and other stuff to work correctly.

During the conference call Elon Musk described the Model X as perhaps the most complicated car ever built – ergo, we’re expecting they’re having some trouble getting the falcon wing doors and other stuff to work correctly.

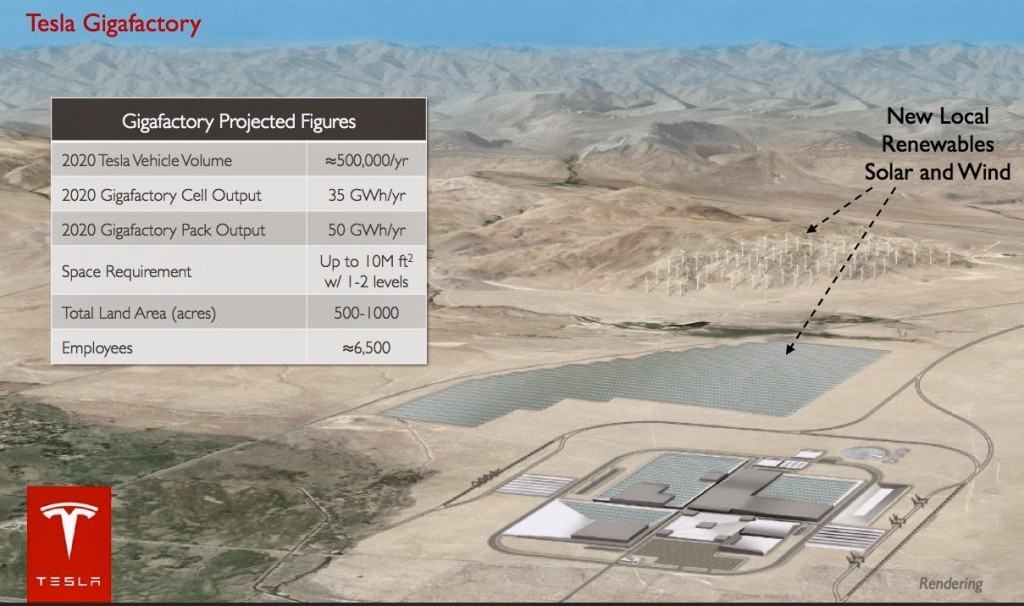

As Model X sales kick in, Tesla’s revenue figures should shoot up considerably. Then next year as the Gigafactory starts production, they’ll start shipping the Tesla Energy products which will boost the revenue even more.

In other words, Tesla Motors has 2-3 quarters of cash on hand (at the current cash burn rate) and the revenue boost from sales of new products (Model X, Tesla Energy) might not be as much as expected. Does that imply a possible cash crunch at the end of the year?

The remedy? An offering of 2.6 million shares which should reap about $600 million to Tesla’s coffers. Or, at the current cash burn rate, about 1.5 quarters worth of cash.

That cash burn rate, however, is because of the capital expenses required to build out the Gigafactory and the Fremont factory so that Tesla Motors can build these new products, and gain new revenue. Which means Tesla’s cash burn rate should decrease significantly by early next year.

We shouldn’t be surprised that Tesla Motors had to do this new round of selling shares to raise money. The road they’re on is immensely difficult – not only are they designing and tooling for two new cars simultaneously (the Tesla Model X and Model 3), they’re building a complicated component supply chain, designing and tooling for Tesla Energy products, and building out a worldwide proprietary charging network.

It all hinges on how the reality of operating the Gigafactory makes battery costs fall as expected. The Tesla Energy products are interesting primarily for their price point – as well as the Model 3. Tesla Motors needs to make a profit on those products to continue funding the company’s growth. If it all works out the sky-high valuation will be justified.

- The USA should delete Musk from power, Instead of deleting whole agencies as he demands - February 14, 2025

- Elon Musk, fiduciary duties, his six companies PLUS his political activities - February 10, 2025

- Is there enough Grid Capacity for Hydrogen Fuel Cell or Battery Electric cars? - April 23, 2023

- Is Tesla finagling to grab federal NEVI dollars for Supercharger network? - November 15, 2022

- Tesla announces the North American Charging Standard charging connector - November 11, 2022

- Lightning Motorcycles adopts Silicon battery, 5 minute charge time gives 135 miles range - November 9, 2022

- Tesla Autopilot under US Dept of Transportation scrutiny - June 13, 2022

- Spectacular CNG bus fire misrepresented as EV bus fire - April 21, 2022

- Moldova, Ukraine, Georgia, Russia, and the European Energy Crisis - December 21, 2021

- Li-Bridge leading the USA across lithium battery chasm - October 29, 2021